I Know Exactly What Pipe Will Break: The Next Systemic Banking Crisis

The law of unintended consequences looms large in economic policy. What may seem today like a benign decision is just as likely to unleash a pandora’s box sometime in the future. When policy is made at the barrel of a gun, transforming the unconventional into the conventional, the risk that a decision might backfire rises exponentially.

When the Federal Reserve implemented the Reverse Repurchase facility (RRP) in September of 2013, it did so because it faced a crisis caused by too much money. The Fed could no longer control the short term interest rate through open market operations in the Fed Funds market alone. Rather, it decided to pay interest directly not just to banks' reserve balances, but also it would create a new facility where money market funds (MMFs) could deposit balances directly with the Fed and get paid interest (via a repo transaction directly with the Fed).

As you might have guessed by my barely concealed foreshadowing, the creation of the RRP solved one near term problem by creating a long term problem. The interesting thing is that when I first started studying the RRP, I originally was most concerned about what would happen if the RRP take-up dwindled to zero. But now I don’t think it will necessarily reach zero at all. To start to understand why, let’s really break down what happens at the Fed’s balance sheet when a MMF deposits money in RRP.

I present exhibit A, according to the Fed’s Liberty Street Economics blog:

An ON RRP transaction—which is economically similar to a secured loan—does not change the size of the Fed’s balance sheet but does shift the composition of the Fed’s liabilities. For instance, when a money market fund reduces overnight deposits with a bank and directs those funds to the ON RRP facility, the increase in the ON RRP facility decreases reserve balances held by banks at the Fed.

To reiterate: an increase in RRP leads to a decrease in the banks’ overall reserve balances held at the Fed. In contrast, a decrease in RRP leads to an increase in reserves. It’s purely an accounting identity; they must offset one another.

So what's the problem?

The problem is MMFs assets are growing and reserves are shrinking…

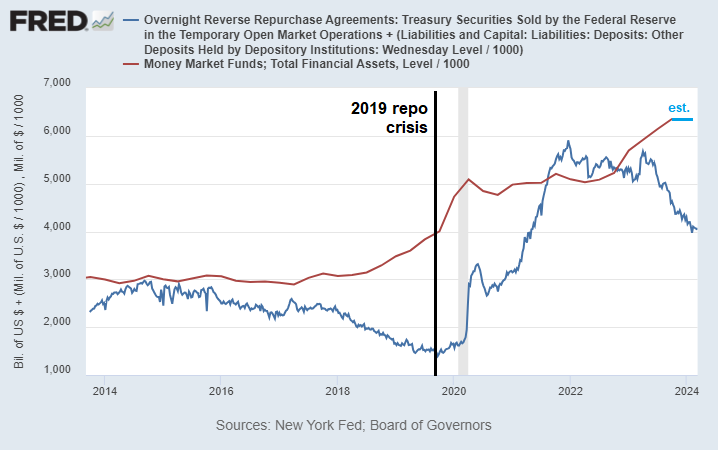

Currently MMF AUM is estimated by ICI to be $6.07 trillion. This stands in contrast to only $4.06 trillion in bank reserves + RRP balances.

The Richmond Fed has estimated that “ample reserves” will become scarce when reserves + RRP are somewhere in the $2.0-3.0 trillion range.

Therefore, if MMFs were to, for whatever reasons, move $1-1.5 trillion in quick fashion from reserves to RRP, we would move rapidly from having too many reserves to having too little.

This could cause a chain reaction where SOFR spikes as there's less MMFs to finance private repo. Left unchecked, i.e. if the Fed did not immediately lend reserves to the banks, this would lead to a mechanical deleveraging event as banks were forced to reduce their own balance sheets as leverage ratios exploded.

Why might the MMFs suddenly shift a trillion dollars from the outside banking system (i.e. private banks) to the inside at the Fed?

Because in 2020 the MMFs were the subject of their own bank run of sorts. Spooked by the global implications of Covid-19, investors pulled trillions of dollars from MMFs. The funds then found themselves short money for redemptions and would have had to dump their assets for fire sale prices had the Fed not bailed out the MMFs.

Once burned, twice shy they say. If MMFs suddenly lose confidence in either the private banks or the federal government they could “withdraw” from the outside banking system and make a “deposit” in the RRP facility at the Fed…

Neither of these losses of faith are unthinkable. The private banks are sitting on top of a barely contained dumpster fire in commercial real estate, and the federal government literally can't stop playing chicken with the nation's finances.

Back in March 2023, big uninsured depositors (e.g. MMFs and stablecoins) caused a run on Silvergate Bank and SVB.

While some depositors fled to the safety of bigger private banks, some 300 billion flowed into RRP from Feb 1st 2023 to the height of the crisis in late March (see chart). The Fed’s response to the crisis was, as always, to create money. That is the only response they credibly have to such an event: to print money in proportion to the size of the crisis.

The flight to RRP in March 2023 was quickly contained because the damage to the private banking system was really localized to banks that dealt with doomed crypto exchange FTX and their founder’s ecosystem of failure.

The second flight to RRP will be much worse because it will be caused by something far more systemic and far reaching into the economy than crypto, such as a sharp drop in an overvalued bubblicious stock market. That or the revelation that some global systemically important bank is in over its head with bad CRE loans. It is worth also noting that the 2019 repo crisis was catalyzed by a 7 year treasury auction that “tailed” badly.

Whatever sparks the deluge, the pipe that will break is the one between bank reserves and RRP. Taken to its extreme, if every MMF yanked their money from the banks and parked it in RRP, bank reserves would have to go negative. Either that or the Fed prints money. Or eliminates RRP and loses the ability to raise rates and the MMFs drive the front end significantly below the Fed’s target range. Either way it's a nasty poison to pick when inflation is still way above 2%.

| A guest post by

|